So it isn't even all "index funds" but S&P 500 indexed funds - which should be about ~40% of all passive index funds. (The "total market" funds, the large-cap funds and the tech funds already include TSLA.)

S&P 500 funds are I think about 5% of shares of high tech firms, which on TSLA would be about 7% of the float: a substantial (and temporary) pop of $50-$100 but probably not "technical short squeeze" material.

(BTW., the smartest index fund arbitrageurs are probably already buying, S&P 500 inclusion next year is probable at this point.)

I'm unsure what you find crazy about what I wrote, the 2013 TSLA short squeeze is a simple historic fact:

Shorts often try to argue that 2013 was different in that "days to cover" was higher. What their argument is missing is that today about 80% of the TSLA intraday volume is HFT/algo trading that doesn't offer liquidity to 30 million shares shorts covering.

I.e. the true "days to cover" is in reality 5 times larger than listed: instead of the

~3 "days to short cover" listed by NASDAQ, the real number is closer to 15 days - and even that is using up 100% of true liquidity to cover, while in reality any such sustained momentum would attract a lot of momentum traders with which shorts would have to compete.

The real time it will take for shorts to cover at naturally available liquidity is closer to 30-60 days. Anything beyond that rate of flow will bid up the price rather significantly - i.e. a short squeeze.

Also, there are several types of short squeezers:

- A "technical short squeeze" similar to the VW short squeeze of 2008 which was violent and over in 2-3 days is unlikely for TSLA, unless a big investor is really bullish and ties up a significant part of the Tesla float.

- A "fundamentals driven short squeeze" is highly probable after Q3 results: the fundamentals of Tesla just improved immensely (cash generation ability close to Apple's and twice that of Amazon, in a much bigger market with a lot of space to grow), which is unlocking a much broader base of investors. The 2013 Tesla short squeeze was such a fundamentals driven short squeeze.

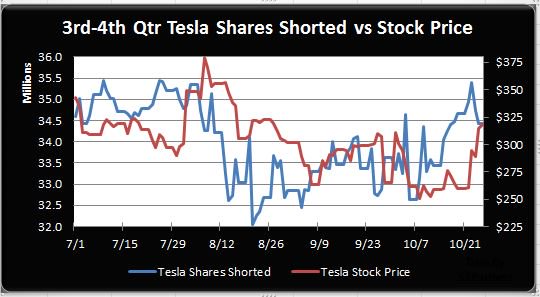

These estimates of mine roughly match what Ihor Dusaniwsky's daily short interest report is showing:

Shorts covered about ~1 million shares since their peak, while the price was bid up by about ~$60. If we naively assume that a third of the price action was shorts covering and extrapolate that to say 30 million short shares covered, that's a price effect of +$600, quite some rocket fuel which would bring the stock to near $1,000 levels if longs didn't change behavior as prices increase - but in reality longs and even long term investors will probably jump in sooner than that to take profits or to swing-trade once they think the short squeeze has been exhausted, or if they think the price levels are irresistible.

Even without a technical short squeeze some nice intraday price action is also possible at around key price levels of short capitulation: I'd not be surprised to see a massive cascade of stop orders once $390 is breached, to well above $400.

There's also some key upcoming events that will unlock even more tiers of investors, such as the Moody's upgrade and the S&P 500 inclusion next year as

@neroden suggested, and of course the upcoming "profitable 18'Q4" event, the "profitable 19'Q1" event, the "profitable 19'Q2" event, etc.. The time frame of the 2013 short squeeze was 6-9 months.

Anyway, all the data suggests that it's pretty probable at this point that there's a

lot of pain waiting for shorts and the price levels at which they will be allowed out of their positions will be determined by Tesla shareholders, not by anti-shareholders.