It'll still come a Tesla because about 8 people will actually buy a Mercedes and use their system. It takes months and a few hundred miles for people to trust a tesla even though the system is actually a good system. No one will engage the Mercedes system after the first disengagement going 500 ft.Well, at least those who keep worrying about "What will happen after the first autonomous fatality" are now more likely to get their answer, only it may come from an incident with a Mercedes rather than a Tesla.

Welcome to Tesla Motors Club

Discuss Tesla's Model S, Model 3, Model X, Model Y, Cybertruck, Roadster and More.

Register

Install the app

How to install the app on iOS

You can install our site as a web app on your iOS device by utilizing the Add to Home Screen feature in Safari. Please see this thread for more details on this.

Note: This feature may not be available in some browsers.

-

Want to remove ads? Register an account and login to see fewer ads, and become a Supporting Member to remove almost all ads.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Tesla, TSLA & the Investment World: the Perpetual Investors' Roundtable

- Thread starter AudubonB

- Start date

Todd Burch

14-Year Member

Not only that, but when people feel like they need to be tighter with their spending, they are less likely to spend on a new technology that they are not fully comfortable with yet--even though this is a quite irrational decision (EVs have been prevalent for over a decade now, and almost everyone who drives them ends up preferring them--and Tesla's customer retention rate is among the highest (or possibly the highest? Can't remember) in the industry).People who can afford expensive ICE generally don't need auto loans. Interest rates have had a big impact on the auto market (and housing).

The smallest amount of range anxiety, regardless of how small that problem is in reality (how would they know?...they've never driven an EV before) will retreat and stick to something they already know (ICE vehicles) instead of taking a risk when they feel that money is harder to come by.

Knightshade

Well-Known Member

The loophole comes from the garbage SAE that doesn't clearly define capabilities and yet assign them levels in which you can have extremely capable autonomous features as L2 and garbage capable systems as L3. The public doesn't understand this so mercedes having zero problem advertising their cars are the first L3 as if it has more capabilities than any autonomous systems out there. How is this not a BS loophole?

You don't seem to understand what the word loophole means my dude.

Definition of LOOPHOLE

a means of escape; especially : an ambiguity or omission in the text through which the intent of a statute, contract, or obligation may be evaded; a small opening through which small arms may be fired; a similar opening to admit light and air or to permit observation… See the full definition

www.merriam-webster.com

www.merriam-webster.com

Definition of loophole said:a means of escape

especially : an ambiguity or omission in the text through which the intent of a statute, contract, or obligation may be evaded

What intent or obligation of J3016 (the statute in this case though it's not a law) specifically is Mercedes evading?

Nor, as we've long established, do you understand what J3016 and the SAE levels are even for-- which seems to be why you think there IS such a loophole. There's not though and your inability to specifically articulate one makes it clear.

None of which has anything to do with how dishonest Omars video is though- so maybe stop trying to deflect your unreasonable defense of it to other topics?

If someone made a video of basic AP not stopping for red lights and labeled each such failure as an intervention--- would you think that's fair and reasonable?

Because that's the same thing Omar did.

Why are you NOT ok with the SAME technique if it makes Tesla look bad-- but FINE with it when it makes Tesla look good?

If mercedes L2 can drive as well as a Tesla and designate a special circumstance for L3, then sure I concede this type of marketing is not misleading.

Again- WHICH marketing? Specifically?

Also "drive as well" isn't a thing.

This again is people thinking the only difference between levels is "how well they drive"

it's fundamentally not

It's actually dangerous for someone who has experienced FSD L2 and thinks their brand new L3 mercedes will be as good if not better, then gets T-boned at a red light.

In exactly the same way it was dangerous for people who died on basic autopilot on city streets.

If someone can't be bothered to read the manual and understand the ODD of a system, that's on them

But an especially confusing bit of the video is this---- Mercedes L3 system is supposed to not even let you turn it on outside it's ODD.

There's a number of videos showing that.

Yet Omars "test" car did.

In fact the other guy in the car specifically calls out the fact he's surprised it turned on there as it's not supposed to.

Would you change your opinion of his video if you found out the car was hacked somehow to let him turn it on on city streets?

(I don't KNOW that for a fact- but either it's that, or there's a major bug in ODD detection-- or 3rd option they're not ACTUALLY showing you the L3 system there at all and just letting folks assume it is)

Last edited:

Exactly my point, people don't understand SAE levels. Everyone associates the levels with capabilities because no one actually read the SAE definitions beside us FSD nerds. Car manufacturers has a marketing department who fully understands this so they pushed Mercedes to...and according to their websiteYou don't seem to understand what the word loophole means my dude.

Nor, as we've long established, do you understand what J3016 and the SAE levels are even for

None of which has anything to do with how dishonest Omars video is though- so maybe stop trying to deflect your unreasonable defense of it to other topics?

If someone made a video of basic AP not stopping for red lights and labeled each such failure as an intervention--- would you think that's fair and reasonable?

Because that's the same thing Omar did.

Why are you NOT ok with the SAME technique if it makes Tesla look bad-- but FINE with it when it makes Tesla look good?

Again- WHICH marketing? Specifically?

Also "drive as well" isn't a thing.

This again is people thinking the only difference between levels is "how well they drive"

it's fundamentally not

In exactly the same way it was dangerous for people who died on basic autopilot on city streets.

If someone can't be bothered to read the manual and understand the ODD of a system, that's on them

"

Next level automated driving.

Raising the bar in autonomous driving technology, Mercedes-Benz is the first automobile manufacturer in the US to achieve a Level 3 certification based on a 0-5 scale from the Society of Automotive Engineers (SAE)1. Under specific conditions, our technology allows drivers to take their hands off the steering wheel, eyes off the road — and take in their surroundings2.While active, DRIVE PILOT unlocks activities on the central display so the driver can play games, watch videos or take advantage of in-car entertainment features.

Capable of detecting your surroundings, conditionally automated vehicles can make informed decisions for themselves. However, these vehicles require the driver to remain alert and take control when requested."

NEXT LEVEL. Not Level 2 like those lame Teslas, but NEXT LEVEL. Mercedes have raised the bar here on autonomy. Just days after their L3 certification, we get plethora of headlines making fun of Tesla's L2 and pointing Mercedes as the true innovator in this space.

This was all by design to take advantage of the fact that SAE never defined or designated each levels with mandatory capabilities. This is a LOOPHOLE per your definition.. " an ambiguity or omission in the text through which the intent of a statute", so stop defending this BS. Omar should continue to expose their BS.

Last edited:

If the car company is not operating well and generating solid profits to pay for these gambles then 2035 is a long way from here.Oh Tesla's best growth is certainly yet ahead of it. The potential of the auto market for Tesla is small (even if they somehow get to 20 million cars/yr) compared to what autonomy and humanoids will earn Tesla down the road. Robotaxi potential is at least a 5X over auto sales, and Optimus is much more than that. Both will have recurring revenues from softwares over massive hardware fleets. Heck Megapack sales alone will be more than the autos make in time.

This isn't happening next year mind you, this is a very long term outlook. Like 2030-2035 timeframe at best, but Tesla today is very small financially compared to where its going.

If you don't believe that then you haven't done enough research nor have you modeled it out. Seeing the potential numbers, the probable earnings, its staggering. There are very good reasons why so many investors are holding for the next decade, and its got absolutely bupkis to do with selling cars.

Knightshade

Well-Known Member

Exactly my point, people don't understand SAE levels. Everyone associates the levels with capabilities.

So the fact people refuse to read the rules means someone following the rules is using a "loophole"?

That's.... not at all what loophole means.

Car manufacturers has a marketing department who fully understands this so they pushed Mercedes to...and according to their website

"

Next level automated driving.

Raising the bar in autonomous driving technology, Mercedes-Benz is the first automobile manufacturer in the US to achieve a Level 3 certification based on a 0-5 scale from the Society of Automotive Engineers (SAE)1. Under specific conditions, our technology allows drivers to take their hands off the steering wheel, eyes off the road

100% of which is factually true.

They even call out it's only under specific conditions

Lemme guess- nobody reads that either (even though it's the specific wording you claim is deceptive despite being 100% accurate)

While active, DRIVE PILOT unlocks activities on the central display so the driver can play games, watch videos or take advantage of in-car entertainment features.

Capable of detecting your surroundings, conditionally automated vehicles can make informed decisions for themselves. However, these vehicles require the driver to remain alert and take control when requested."

Right- again all factually accurate. CONDITIONALLY automated. Meaning only under specific conditions-- so they call this out TWICE in the description.

NEXT LEVEL. Not Level 2 like those lame Teslas, but NEXT LEVEL.

Making up things Mercedes didn't say to attack the accurate things they did is....not useful.

This was all by design so stop defending this BS. Omar should continue to expose their BS.

The only BS is the video itself dishonestly using a system outside its ODD and then citing "interventions" for things the system's not meant to even do.

Oh, and also your defense of said video despite every actual fact showing you otherwise.

Bullish doesn't have to mean willing to be dishonest to make Tesla look better.

rentierparasit

Member

Hi, Unk --The market discrepancies are largely explained by income distributions, taking the US example:

Even though that 2022 data should a modest decrease in income inequality;

Income in the United States: 2022

This report presents data on income, earnings, & income inequality in the United States based on information collected in the 2023 and earlier CPS ASEC.www.census.gov

The effects of the income stability at the top 5% with increased pressure on the middle 40% or so is visible in market changes in 2023/2024, even though the historical published data has not yet displayed that. To be sure, unemployment data and inflation numbers are factors, but are indirect ones.

In nearly all categories reflecting the highest income and wealth categories there is clear evidence that sector is not suffering:

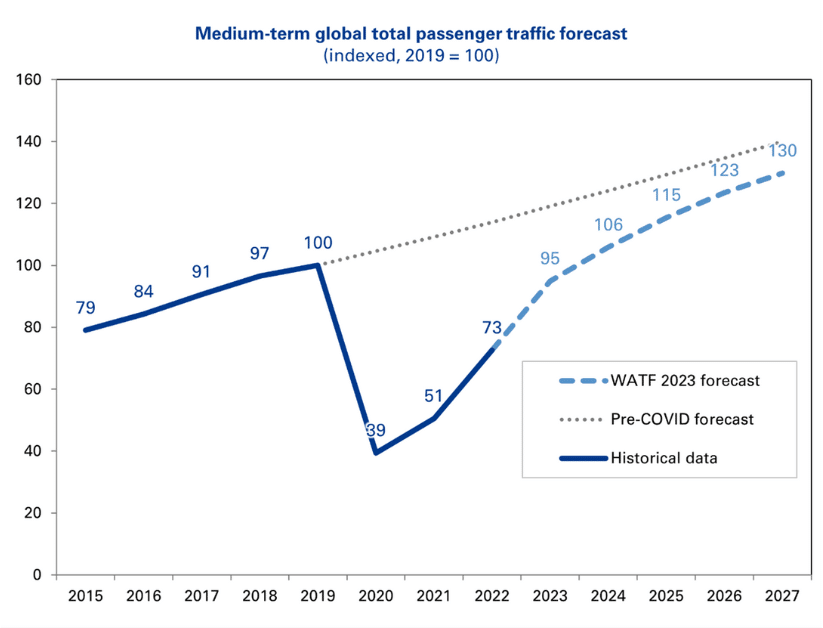

Business jet demand is usually a good indicator of the “View attachment 1046700

The trusted source for air travel demand updates | ACI World

Montreal, 14 February 2024 – Airports Council International (ACI) World has published its first bi-annual air travel demand update of 2024, pulling data fromaci.aero

Overall, in my opinion, global evidence in luxury hotels, air travel etc clearly shows high disposable income for the top income class.

People who fly frequently have all observed overbooked flights packed premium classes almost everywhere here.

So what about auto sales? Elon Musk saw the decline coming and said it well before it happened. Why was this surprising to anyone is a different question. First, through Covid-19 and supply dhortsges TSLA proved superior logistics, outstanding supply chain management and highly flexible manufacturing allow simply powering through while others suffered.

Then 2023 delivered multiple very difficult situations from, in US alone NHTSA, formal EV conference excluding Tesla. Elsewhere repeated Terrorist threats, IG Metall began… and…The equanimity-shattering political situations exacerbated by the Feb 2024 Delaware Chancery Court infamous decision.

All of that partly explains EV pressures, explains distraction at Tesla, but is not the global loser-range vehicle sales issues.

Those all are more nearly the result of abnormal pent-up demand almost globally in late 2022-2023 and post-pandemic demands drove demand . The missing link, in my opinion, is the effects of COVID-19:

- every aspect of home delivery has, almost around the globe, had lasting impact on purchasing, as people simply drive less, using delivery for food, consumer goods, even many medical services. That in turn has the direct effect of reducing personal vehicle demand.

- ride sharing (Uber etc) has vastly reduced usage of personal vehicles while not having direct measurable effect on owning them.

These are all cumulative and each might have negligible effects, but the aggregate of these is huge.

Those who are convinced of Robotaxi see almost all of these as evidence for mass adoption. They are all evidence of gradually weakening demand for less affluent people to buy cars.

None of the markets are disappearing. The traditional new vehicle sales among less affluent people are, unquestionably, reducing in size and purchasing capacity.

Just glance at the progression of incentives in Automotive News both US and Europe, and a national data elsewhere. The developments are clear.

Then think about how distracted Tesla CEO may have been last year.

Interesting, but I'm not sure on the read-through to Tesla. YTD, global auto sales are up; EV sales are up, with PHEV outperforming BEV, but BEV is still up; but Tesla is down. So, to me it's share loss that requires explanation. I guess you could argue that, because Tesla disproportionately benefitted from COVID/Ukraine disruptions, they'll be disproportionately affected by the unwind? Is that what you're getting at?

Yours,

RP

Omar is exposing what everyone who understands all this knew from the beginning. Mercedes tried to make themselves look better when their autonomous program is 95% marketing and 5% substance.So the fact people refuse to read the rules means someone following the rules is using a "loophole"?

That's.... not at all what loophole means.

100% of which is factually true.

They even call out it's only under specific conditions

Lemme guess- nobody reads that either (even though it's the specific wording you claim is deceptive despite being 100% accurate)

Right- again all factually accurate. CONDITIONALLY automated. Meaning only under specific conditions-- so they call this out TWICE in the description.

Making up things Mercedes didn't say to attack the accurate things they did is....not useful.

The only BS is the video itself dishonestly using a system outside its ODD and then citing "interventions" for things the system's not meant to even do.

Oh, and also your defense of said video despite every actual fact showing you otherwise.

Bullish doesn't have to mean willing to be dishonest to make Tesla look better.

Now, if Mercedes were not so quick to certify as a L3 trying to market themselves as the leader when their system is trash, and CR didn't give so much praise to their systems...then YES, Omar was extremely unfair to the Mercedes system. But this is not what happened. I have no problem with people showing FSD mistakes exposing Elon for making FSD being more than what it is.

You must be hoping people read your post but not the "article" - excuse me, "paragraph".

Tesla's Model 2 reportedly shelved just before completion

Tesla Inc. and SpaceX Chief Executive Officer (CEO) and X Corp. Chairman Elon Musk canceled the production of the electric vehicle (EV) company's Model 2 when it was nearly done, The Information repor...breakingthenews.net

More news today of the Model 2 cancellation/shelving/insert term here.

It's just a mention of what is now month old news, nothing new about it. No "news today" at all.

I believe you must have mistakenly posted to an article that doesn't support your claim. You may want to check that. Maybe read what you link before posting?

Not a criticism, hoping to be "helpful". You don't want to damage your reputation here!

cliff harris

Member

Mercedes system only works on certain roads. Thats not self-driving, thats 'driving on certain roads'. For all practical purposes they may as well just given free train tickets to mercedes buyers who live near specific roads.

If people are going to let mercedes get away with claiming they sell self driving cars but only on certain roads, then Tesla should rename Full Self Driving to Universal Self Driving, to show how it can be enabled even on (shock horror) roads that have not been visited by and mapped and approved by a bunch of Mercedes engineers.

Anybody who thinks any sort of autonomous system that is dependent on HD maps and road-approval poses ANY threat to FSD is just delusional (or a paid troll). Even apple wouldn't sell a car that only drove on iRoads.

If people are going to let mercedes get away with claiming they sell self driving cars but only on certain roads, then Tesla should rename Full Self Driving to Universal Self Driving, to show how it can be enabled even on (shock horror) roads that have not been visited by and mapped and approved by a bunch of Mercedes engineers.

Anybody who thinks any sort of autonomous system that is dependent on HD maps and road-approval poses ANY threat to FSD is just delusional (or a paid troll). Even apple wouldn't sell a car that only drove on iRoads.

Knightshade

Well-Known Member

Omar is exposing what everyone who understands all this knew from the beginning

That his videos misrepresent the facts and can't be trusted?

Sure, but we've known that for years- hardly the first time he was dishonest in a video about self driving--- and why repost such trash here?

. Mercedes tried to make themselves look better

How?

NOTHING in Omars video is about what mercedes said about anything except the parts where the other dude in the car keeps pointing out they're using it in conditions Mercedes says it's not meant to work but Omar keeps counting as "interventions" anyway.

If I pushed out a video where I only enabled dumb cruise control on a car-- then counted as "interventions" every time I had to hit the brake to not hit a car in front of me- would that seem a reasonable use of anyone's time or an attempt at any sort of honest point? That's what he did here.

Notice how -0 percent- of the video is on an actual highway? Because he's intentionally doing all he can to operate the system where it's not intended and make it look bad.... then he doubles down when the other dude tries to make the reasonable point it's ONLY FOR HIGHWAYS and Omar tries to tell him "Any road is a highway if you're doing 45".... what?

Now, if Mercedes were not so quick to certify as a L3

But the system IS LEVEL 3.

The fact your refuse to learn what that even means is not Mercedes problem- it's yours.

trying to market themselves as the leader when their system is trash, and CR didn't give so much praise to their systems...then YES, Omar was extremely unfair to the Mercedes system.

What CR said or didn't say has nothing to do with OMAR being dishonest in the video my dude.

Your argument has now distilled down to "I don't like what others said about Tesla, so I'm fine if other pro-Tesla people say dishonest things in response"

That's a garbage argument.

Why are you making it?

Last edited:

2daMoon

Mostly Harmless

You must be hoping people read your post but not the "article" - excuse me, "paragraph".

It's just a mention of what is now month old news, nothing new about it. No "news today" at all.

I believe you must have mistakenly posted to an article that doesn't support your claim. You may want to check that. Maybe read what you link before posting?

Not a criticism, hoping to be "helpful". You don't want to damage your reputation here!

But, don't they still get paid for generating a response?

Whoops, two responses...

If the car company is not operating well and generating solid profits to pay for these gambles then 2035 is a long way from here.

This one of my short term worries about Tesla: can the auto part of the business still financially enable the company to invest into deploying the RT fleet?

We've seen Tesla slowing auto production, possibly changing the Model 2 into an economy 3/Y variant, dropping auto margins to razor thin levels, reducing labor force and SC resources. 20 million cars per year by 2030 now seems impossible, and I've no idea what the actual production number will be by then anymore. My best prediction is more like 8 million by 2030 given the slowed buildout of factories and production lines, including RT's produced. Will these changes provide enough revenues to spend on completing FSD and building an RT fleet? I hope so.

I'd love to see a renewed push into accelerating Megapack production to offset the reduced auto incomes. Long term this might mean Tesla simply moves slower from here on out, I'm not sure.

Knightshade

Well-Known Member

Mercedes system only works on certain roads. Thats not self-driving

It literally and legally is though.

Specifically L3- conditional self driving.

Exactly the words Mercedes writes in describing the feature. Condition. Under specific conditions. And exactly what SAE defines as L3.

If people are going to let mercedes get away with claiming they sell self driving cars but only on certain roads, then Tesla should rename Full Self Driving to Universal Self Driving, to show how it can be enabled even on (shock horror) roads that have not been visited by and mapped and approved by a bunch of Mercedes engineers.

Except Teslas system is not self driving on any of those roads- because it always requries a human to be actively performing part of the driving task.

Mercedes system, under specific conditions, does not

This doesn't mean one is "better"- it means they factually function differently.

SAE levels are not "scores"

Anybody who thinks any sort of autonomous system that is dependent on HD maps and road-approval poses ANY threat to FSD is just delusional (or a paid troll). Even apple wouldn't sell a car that only drove on iRoads.

This is a totally different discussion.

Teslas system is vastly more USEFUL to most people.

Mercedes system is definitionally autonomous SOME of the time. Teslas NEVER is in current state. That's an actual, legal, distinction.

lafrisbee

Active Member

My main rebuttal has been I did invest, and I will invest. My decisions are not any different than an investor. I look at the actual facts that are real world/market to decide when and where to invest. I do not look at market metrics, which is how I differentiate between an investor and a trader.Is this difference in perspective all that surprising when one is that of a shareholder and the other is that of someone who sold most/all of their shares?

You made your choice, what is to be gained by trying to justify your decision to those who held through the bottom?

Since the time when you sold, your posts have sounded more and more like it is really you whom you want most to be convinced.

Apologies for the absence of confirmation bias being offered here. It seems unlikely that making more posts like these will change this.

Besides, with the power that Market-money makers have with TSLA it is stupid to be a trader unless you are one of the Money/market makers.

nativewolf

Active Member

Omar normally just produces stupid videos pumping Tesla developing automation, which is fine, they are completely disingenuous but that is what he does and anyone that has seen his "FSD is around the corner" video from half a decade ago knows this. This latest thing is a below the belt hack job of the worst sort. There is nothing to defend @Singuy . It's a hackjob. No need to get into a definitional war with Knightshade because ..it's a hack job of the worst sort. He could just as easily done a great video showing that MB system works just fine but only in the conditions constrained by it's L3 capability (which is very limited). Then he could show all the things it can't do. That would all be above board. Instead he put together a shameful video that really doesn't help Tesla and simply makes Tesla look weak & useless. If you resort to that sort of Dowd like behavior who wants to be associated with it. You lose credibility when you defend something that is obviously shameful, IMO.That his videos misrepresent the facts and can't be trusted?

Sure, but we've known that for years- hardly the first time he was dishonest in a video about self driving--- and why repost such trash here?

How?

NOTHING in Omars video is about what mercedes said about anything.

On the contrary, the other guy in the car points out- more than once- Omar is instead using Mercedes system in conditions Mercedes themselves tells you not to.

But the system IS LEVEL 3.

The fact your refuse to learn what that even means is not Mercedes problem- it's yours.

What CR said or didn't say has nothing to do with OMAR being dishonest in the video my dude.

Your argument has now distilled down to "I don't like what others said about Tesla, so I'm fine if other pro-Tesla people say dishonest things in response"

That's a garbage argument.

Why are you making it?

Webeevdrivers

Active Member

I think 8 million is pie in the sky. Maybe 3 or 4 million. And that’s only if they expand quickly into untapped markets like South America.This one of my short term worries about Tesla: can the auto part of the business still financially enable the company to invest into deploying the RT fleet?

We've seen Tesla slowing auto production, possibly changing the Model 2 into an economy 3/Y variant, dropping auto margins to razor thin levels, reducing labor force and SC resources. 20 million cars per year by 2030 now seems impossible, and I've no idea what the actual production number will be by then anymore. My best prediction is more like 8 million by 2030 given the slowed buildout of factories and production lines, including RT's produced. Will these changes provide enough revenues to spend on completing FSD and building an RT fleet? I hope so.

I'd love to see a renewed push into accelerating Megapack production to offset the reduced auto incomes. Long term this might mean Tesla simply moves slower from here on out, I'm not sure.

The ticket will be finding markets where they don’t associate Tesla with Elon. That’s just the way it is now. At some point even tesla will have to recognize that.

I think tesla could still be a good and profitable company at those levels. Just not the industry behemoth everyone thought it would be.

Jmho.

cliff harris

Member

The trouble with fighting about rival self driving systems using real time video is that its not a single drive that is the problem. I'm sure its perfectly possible to do a 90 minute Mercedes drive that is flawless. That would make for a great stock-pump video.

The problem is, if you only have a catastrophic crash that kills your children with an autonomous car every thousand miles... thats still probably quite an issue, but it would make for a very tedious 40 hour long video.

The one thing Tesla has that nobody else has, is the freedom and confidence to say "here is your one month free trial. Drive using FSD anywhere, any time, in any weather, and you decide how reliable it is."

Thats not a phrase a mercedes salesperson will be using with any confidence.

The problem is, if you only have a catastrophic crash that kills your children with an autonomous car every thousand miles... thats still probably quite an issue, but it would make for a very tedious 40 hour long video.

The one thing Tesla has that nobody else has, is the freedom and confidence to say "here is your one month free trial. Drive using FSD anywhere, any time, in any weather, and you decide how reliable it is."

Thats not a phrase a mercedes salesperson will be using with any confidence.

Mercedes

Required operating conditions

Building over a century of trust in drivers across the globe begins and ends with safety. DRIVE PILOT is ready to chauffeur you under conditions that help ensure a secure ride. Conditions include:- Clear lane markings on approved freeways

- Moderate to heavy traffic with speeds under 40 MPH

- Daytime lighting and clear weather

- Driver visible by camera located above driver's display

There is no construction zone present.

The 1st oxymoron is to be driving on highways at speeds under 40MPH. It got me

") So just when your commute is stuck.

So just when your commute is stuck.the fact that they advertise for 40MPH and not on city roads at that speed means it's a piece of crap. (there I said it). At least waymo sticks to city streets at these speeds.

What happened to German Engineering and the Autobahn speeds

How is this L3 I don't know? Don't point me to the architecture docs (

, I have read them )Under these conditions Tesla might be L5 +

Street/SPACs definitely scheming to creating the Nikola, Lordstown of FSDs

Last edited:

Similar threads

- Locked

- Replies

- 0

- Views

- 4K

- Locked

- Replies

- 0

- Views

- 6K

- Locked

- Replies

- 11

- Views

- 10K

- Replies

- 6

- Views

- 5K

- Locked

- Poll

- Replies

- 1

- Views

- 12K