You can install our site as a web app on your iOS device by utilizing the Add to Home Screen feature in Safari. Please see this thread for more details on this.

Note: This feature may not be available in some browsers.

Is it maybe share buyback time?

It would be very sensible to do so when Tesla can buy TSLA at its current low value, and we are now looking at $23billion in cash doing not very much. Tesla buying TSLA seems a great way to spend maybe $2billion of that?

It also looks like fears of economic disaster were perhaps a bit overblown? TBH I'm surprised the question didn't come up on the earnings call.

Is it maybe share buyback time?

It would be very sensible to do so when Tesla can buy TSLA at its current low value, and we are now looking at $23billion in cash doing not very much. Tesla buying TSLA seems a great way to spend maybe $2billion of that?

Had a MY loaner from Tesla for four days. Full FSD which I don't have.

First, my app/car connected to this loaner via code in 15 seconds. I could use my phone for the first time with a loaner - I suspect this is the same with Hertz now.

Now, the FSD. 6-7/10 depending on the road/route. It was great on highway with passing and merging. Not bad on major, clearly marked roads/intersections.

Sometimes, it was just bad. No turns, wrong turns, different hwy exits, etc.

So, no - not this year for sure. YMMV.

I see again the reference to the length. (This time that it will fit in a 20 foot garage). But has anyone actually got real measurements yet? (Our garage is bang on 19 feet).

If scrap bill is solely cells that fail at formation (versus scrap at all steps) then the yeild went up also which reduces amortized costs.

If we assume gross volume and gross cost per cell (pre formation) didn't change, then a 25% reduction in cell COGS on a 40% reduction in scrap implies that yeild improved from 55% to 73%, 18% absolute gain or 32% relative.

Say current output cost is $1 per unit. Of that, 60c is scrap and the other 40c is not scrap. If we reduce the scrap cost by 40% then the new scrap cost is about 35c. (60-(.4X60) = 35). If we add the new lower scrap cost of 35c to our not scrap cost of 40c then our total cost per unit is now 75c. 75c per unit is a reduction of 25c or 25% from our original cost ... which is what they say they achieved.

I won't be able to find a source since it was long ago, but from some insider info yields were 80%+ months ago, but that could have been just for Kato Rd. without DBE being used on both anode and cathode

Sure, and ties buyers into perpetual underwater equity. Stupid and dangerous move. Somebody should ahem show Tesla executives the default rates by tenor. The longer the tenor the higher the default rate. The slope and size of that path varies by percentage equity going in, but is always there.

My data is from OEM proprietary sources so I cannot post details. Anybody with access to securitized auto loan portfolio details can find confirmation, although the longest tenors are rarely included in pools. The major rise in loss frequency and severity is in tenors above 60 months, with origination loan value to purchase price and origination interest rate being closely related variables.

Suddenly Hertz might replace Toro as my major Tesla rental choice.

The corporate discount to which I am entitled from them makes them cheaper too.

This will pay off for Hertz, particularly if that let's us use our own app to Supercharge.

Is it maybe share buyback time?

It would be very sensible to do so when Tesla can buy TSLA at its current low value, and we are now looking at $23billion in cash doing not very much. Tesla buying TSLA seems a great way to spend maybe $2billion of that?

It also looks like fears of economic disaster were perhaps a bit overblown? TBH I'm surprised the question didn't come up on the earnings call.

That pile of cash has multiple potential uses, including making the company less vulnerable to adversity.

For example, it is currently heavily dependent on China, which has a government that wants Tesla to lose to Chinese companies like BYD, Volvo, Nio and XPeng. Although Tesla is trying to loosen that dependency, that cash pile is a very important defense.

I don't think so. Another way to look at this is the "40% reduction in scrap lead to a 25% reduction in COGS". Let's refer back to the Sep 2022 Battery Day Slide (pg 48) that explains the cost breakdown for cathode: (the most expensive component of the cell)

"PROCESSING" accounts for 35% of the cost of the cathode, whether it results in a useful cell or in scrap. If you can reduce scrap rate by 40%, you automatically reduce COGS as a percentage because output is now higher.

The COGS percentages would decrease something like this: -0.4*(0.35+0.25+0.05) = -26% or about what Drew said. Obviously, cathode isn't the only component of a cell, but it's the largest cost, and if processing is also about a third of other materials cost, then the above ratio also applies.

Can you (or anyone) remind me how many cell lines are installed at which locations ?

I have a vague memory it is 1 installed & operating at Austin, 3 commissioning at Austin, and 1 (equivalent) operating at Kato ......... but that is just memory

Sure, and ties buyers into perpetual underwater equity. Stupid and dangerous move. Somebody should ahem show Tesla executives the default rates by tenor. The longer the tenor the higher the default rate. The slope and size of that path varies by percentage equity going in, but is always there.

My data is from OEM proprietary sources so I cannot post details. Anybody with access to securitized auto loan portfolio details can find confirmation, although the longest tenors are rarely included in pools. The major rise in loss frequency and severity is in tenors above 60 months, with origination loan value to purchase price and origination interest rate being closely related variables.

I think everyone is aware of that. What changes the equation is fsd. When they enable people to generate revenue from their vehicles the value proposition changes.

Is it maybe share buyback time?

It would be very sensible to do so when Tesla can buy TSLA at its current low value, and we are now looking at $23billion in cash doing not very much. Tesla buying TSLA seems a great way to spend maybe $2billion of that?

It also looks like fears of economic disaster were perhaps a bit overblown? TBH I'm surprised the question didn't come up on the earnings call.

I am not a fan of shared buyback for Tesla. The factory, technological, market and other risks are very large, as is the negative consequences of being profligate with capital. A large part of the Tesla success story is a positive cash generation cycle, virtually unprecedented for any industrial company.

Being nearly debt-free except for securitizations is a huge virtue. It would be unwise and imprudent to risk that in the face of huge risks, specifically including environment risks in Fremont and Lathrop from earthquakes and drought, Flooding for Shanghai and so on. These have not yet been major issues for Tesla.

Not yet...

All this encouragement to do share buybacks, lengthening loan tenors and doing broadcast advertising terrifies me. Those are tactics to encourage risk of disaster, not minimize that probability.

I think everyone is aware of that. What changes the equation is fsd. When they enable people to generate revenue from their vehicles the value proposition changes.

Perhaps, but it absolutely will not change risk profiles. Those same characteristics apply for commercial vehicles too, albeit with more complex analytics. Despite assertions and beliefs, FSD sufficient for fully autonomous non-geofenced operations will not happen for at least a decade at best. Why? If the technology were perfect today regulatory reticence alone would delay for a decade or so.

Fully autonomous trains and aircraft can be widespread today. All the technologies are in place. Even so they're limited to freight, localized airport and municipal people movers, and many military applications.

General transportation is not even widely considered. The old saw of commercial flight training has log been that "the aircraft needs one pilot and one dog. The pilot is there to feed the dog. The dog is there to bite the pilot if the pilot reaches for any controls".

'ain't gonna happen anytime soon' not because of technology. The technology is necessary but not sufficient. Elon is thinking about technology, not regulation. Hence, he's incorrect about his expectations.

Say current output cost is $1 per unit. Of that, 60c is scrap and the other 40c is not scrap. If we reduce the scrap cost by 40% then the new scrap cost is about 35c. (60-(.4X60) = 35). If we add the new lower scrap cost of 35c to our not scrap cost of 40c then our total cost per unit is now 75c. 75c per unit is a reduction of 25c or 25% from our original cost ... which is what they say they achieved.

Or 40% scrap reduction then means 36% failure or 64% yeild.

Cogs = $0.40 + 26%/64%*.4 = $0.625

That would be a 37.5% reduction, which means the inital 40% yeild rate was too low.

Going the other way

Cogs=$0.75

0.75=0.4+0.35

.35/.4 = .875 failure per good

1.875 cells gross for 1 cell net

Yeild = 1/1.875 = 53%

Only 7% better or 7/60=12% improvement in scrap. Again showing yeild started too low.

I don't think so. Another way to look at this is the "40% reduction in scrap lead to a 25% reduction in COGS". Let's refer back to the Sep 2022 Battery Day Slide (pg 48) that explains the cost breakdown for cathode: (the most expensive component of the cell)

"PROCESSING" accounts for 35% of the cost of the cathode, whether it results in a useful cell or in scrap. If you can reduce scrap rate by 40%, you automatically reduce COGS as a percentage because output is now higher.

The COGS percentages would decrease something like this: -0.4*(0.35+0.25+0.05) = -26% or about what Drew said. Obviously, cathode isn't the only component of a cell, but it's the largest cost, and if processing is also about a third of other materials cost, then the above ratio also applies.

for a few reasons :

One, the Q3 letter states: "The total number of 4680 cells produced (cells sent to formation) increased 3x sequentially in Q3." So production numbers are based on completed cells (good or bad)

Two: if we allow scrap to be across all processes, we can't calculate yeild.

Three: validation of intermediate steps is difficult to impossible at scale, formation will be the true QC step.

Four: within a process, scrap theoretically only occurs at non reversible steps like coasting. These would be monitored and controlled.

So I see it as a process stack up issue where variability occurs randomly and not systematically such that they can't just tweak and test a single step on its own. They need to tweak, build the cells, test them and then see if things improved.

Catching a failure early reduces additional scrap costs, but I don't follow the rest of your argument.

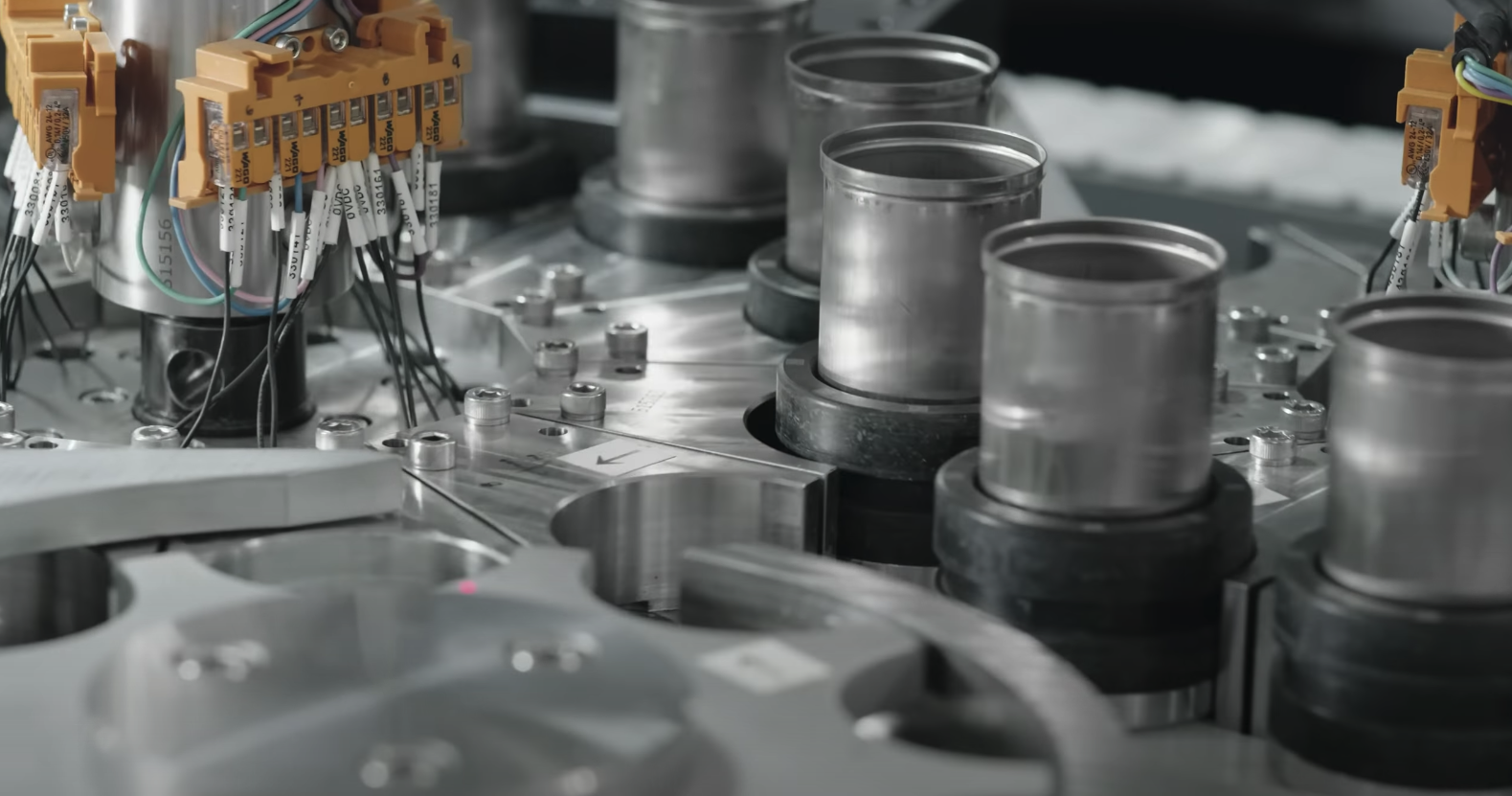

DREW BAGLINO "Yes. First, I’ll just start with a little bit of a production update. So, in Texas, 4680 cell production increased 80% Q2 over Q1, and the team surpassed 10 million production cells produced here in Texas. So, congrats to the team for that. Their focus on yield reduced our scrap bill by 40% quarter-over-quarter, and that resulted in a 25% reduction in cell COGS.

What I asked myself was how high is the scrap rate when the scrap bill is reduced by 40 % and the COGS decreased by 25 %.

I assumed that the recycling of the scrap cells is quite complex unless there is an optimized process in place, therefore I assumed no cost savings in the recycling of cells for my back of napkin calculation.

Q1

Q2

Decrease

Usable Cells

100%

100%

Non Usable Cells

233%

167%

40.0%

Total Cells

333%

267%

25.0%

Yield Rate

30%

38%

I came to the conclusion that the yield rate was approx. 30 % in Q1 and was 38 % in Q2. If my calculation was wrong, please explain how this mathematical problem is actually solved. So I assumed that the yield is still quite poor and my assumption was that it will take time until acceptable yields of lets say 90 % are achieved. This is inline with Drew's quote: "As we scale Cyber cell production through the end of the year and early next, we should be in a comfortable place on cost per cell."

If we assume that the yield is poor, then a scale-up of the production might be still possible but would produce mountains of scrap cells which only can be recycled when there is an established recycling process in place. So this is an argument to actually take the time focusing on refining the process and reducing the scrap rate and this is what I think what Tesla is doing. In the end this speaks for a late Cybertruck start, for example in Q4 2023. This is not what I was hoping for and therefore I described it as "late".

Thanks as well to @MC3OZ in providing more details about past and future improvements in your post.

My take on the 4680 update from Drew was very bullish.

The Cybercell achieved the required energy density for initial CT production essentially via packaging improvements. IMO it is very likely that those improvements are at cell and pack level and an improved structural battery pack design might be very signicantly.

Drew specially said the Cathode and Anode improvements from battery day are not included at this stage. That means there is another up to 24% increase in range that is possible once these improvements can be implemented.

Cathode improvements were always dependent on the Cathode plant that is being built at Austin.

Cost reduction is a function of the cathode plant, the lithium refinery, energy density improvements, and the production ramp with a host of small design and process improvements.

The big advantage of building your own stuff is the opportunity to get better at it, and to bank the profits.

Your calculation @Optimeer seems to me to be fine, but I cannot square the result you present - a yield of approximately 30-38% - with other previous information, and I think I can see how to solve this issue.

If you go back to Jan-2022 there were some leaded Kato Rd yield documents that indicated a 92% yield from a line consisting of 14 machines

Tesla has been working hard at perfecting the production process of their new 4680 battery cells at their facility on Kato Road. The process is a balance between increasing throughput (the number of cells produced) […]

driveteslacanada.ca

I find it difficult to believe that they would knowingly operate at a 30% yield, if they also know how to operate at a 92% yield. Speaking from bitter experience of operating/commissioning process machinery you simply drown in scrap if you turn the rate up before the yield is under control.

The only way I can make sense of Drew's statement is if there is a very significant cost in dealing with reject cells. Setting aside the complexity of how soon in the various stages of production they can identify a dud cell, I can absolutely believe that this is a costly exercise (however much we might wish otherwise). And the more I think about it the more I suspect that they have very little chance of detecting a dud cell before it is fully produced. So the recycling/disposal/etc is by then as expensive as it possibly could be for a single cell (i.e. one that has yet to go in a pack).

Also remember that the machinery installed at Austin has a theoretical design rate of far in excess of the current rate. So does not have to 'solve' the 80% increased production through a yield increase as it is in fact a throughput increase. The scrap and CoGS improvements that Drew stated are (imho) on a cetus paribus basis, for two lines operating at the same production rate.

One cannot be absolutely sure of the actual yields because there are too few pieces of information. But by knowing the scrap improvement we can see the (infinite) possible pair-wise situations, of which here are two that would fit the situation Drew describes. Of course in this example the cost per cell is notional, but the real issue is the relative cost of making vs scrapping a cell.

The 80% rate increase does help in one respect. It enables a fix on the likely Q1 rate from Austin. I'm considering the implications of that.

EDIT : I see @mongo is higlighting much the same thing as I am. But for various reasons I think Tesla are now operating in a high 90s% yield environment, but a very high per cell scrap cost. As I set out above.

There were reports, taken seriously by some in here, that bots were already on the night shift in the factory "freaking out" workers-- so perhaps the question serves to clarify to those folks that it ain't so and we're still some distance away from them either being in large #s or doing useful work.

Can you expand on this? Because it reads like you don't understand what IP theft is, since nothing in the first part of your post is remotely close to it. Turning on a feature in the code running on your car isn't "IP theft" under any legal meaning of the term.

Teslas years-long violations of GPL however pretty clearly are and there's a good decade now of evidence having nothing to do with Green.

Since 2013, the Software Freedom Conservancy (SFC), responding to complaints of GPL violations related to software in the Tesla Model S, has pressed the carmaker to comply with the terms of the GPL.

Some software blueprints doled out after years of complaints

www.theregister.com

That story is from 2018 about them finally making token gestures toward compliance- something they still have failed to do completely another 5 years on.

For someone who so often is mad about market makers ignoring rules it's odd you don't seem to care when Tesla does so.

I've seen a lot of FUD articles about Project 42 (Elon's rumored "glass house") crop up again in the past few days on news sites. These articles are always the same: all conjecture, no evidence of any kind.

Ironically this story always seems to crop up around earnings reports.....must be coincidence though.

. It’s called determination.

. It’s called determination.