Hi fellow Canadians,

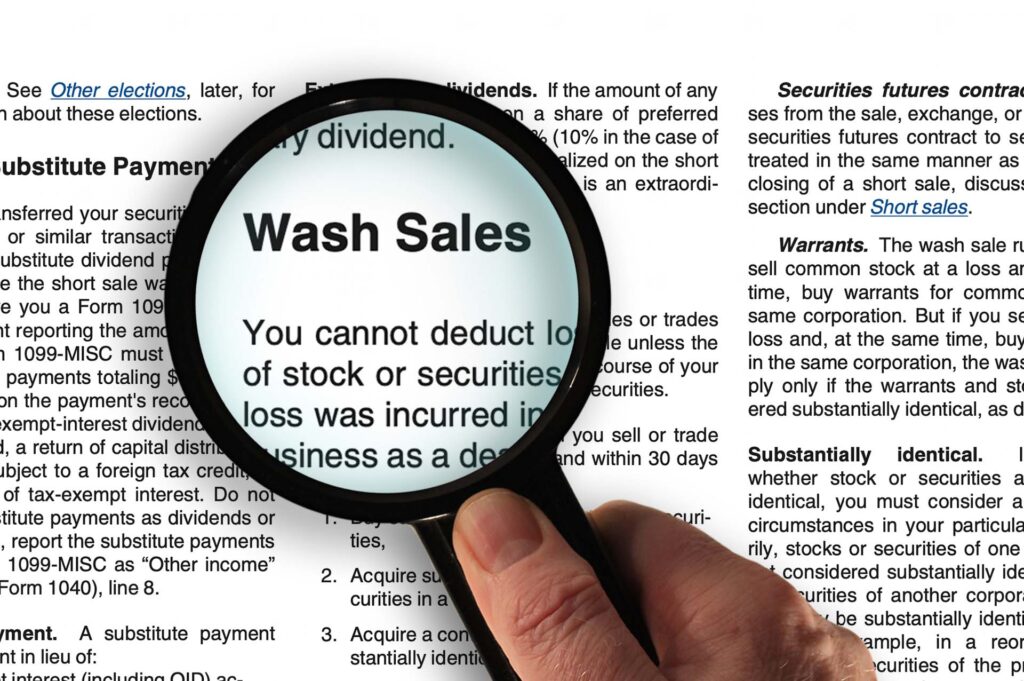

I have been a TSLA Hodler for 5 years before starting option selling in November and have made some profit from option selling in a taxable corporate account. I would like to invite everyone to share how they optimize their taxation so we all finish the year in a better tax situation. I have sold some losers in my Canadian stocks like BBD.B, WEED.TO and HPQ.V which comes to a 150k loss to offset the 150k profits I have made from a selling options and BLU. Do each 1$ of realized losses offset each 1$ of realized profit in option selling? Do you tend to buy back trades gonna bad and underwater the last week of the year to sell them back at the beginning on the following year to minimize impact on taxation?

Please share your strategies here to help others and to avoid clustering the main investors and option selling threads.

Happy Holidays to everyone.

I have been a TSLA Hodler for 5 years before starting option selling in November and have made some profit from option selling in a taxable corporate account. I would like to invite everyone to share how they optimize their taxation so we all finish the year in a better tax situation. I have sold some losers in my Canadian stocks like BBD.B, WEED.TO and HPQ.V which comes to a 150k loss to offset the 150k profits I have made from a selling options and BLU. Do each 1$ of realized losses offset each 1$ of realized profit in option selling? Do you tend to buy back trades gonna bad and underwater the last week of the year to sell them back at the beginning on the following year to minimize impact on taxation?

Please share your strategies here to help others and to avoid clustering the main investors and option selling threads.

Happy Holidays to everyone.